Firefly Aerospace Acquires SciTec for $855M, Supercharges Its Defense & Space Trajectory

By Tredu.com • 10/6/2025

Tredu

Firefly’s Bold Move into Defense: SciTec Acquisition Details

Space- and launch-focused Firefly Aerospace has announced its acquisition of SciTec, a national security tech firm specializing in missile tracking, intelligence, and surveillance systems, for approximately $855 million.

The deal structure comprises $300 million cash and $555 million in Firefly equity (shares). SciTec will continue operating as a Firefly subsidiary under its existing leadership.

This acquisition marks a clear pivot: Firefly is not just a rocket company, it’s staking a claim in the underbelly of defense systems. With SciTec’s software, data analytics, and sensor systems, Firefly positions itself to integrate launch, space, and national security technologies into one consolidated platform.

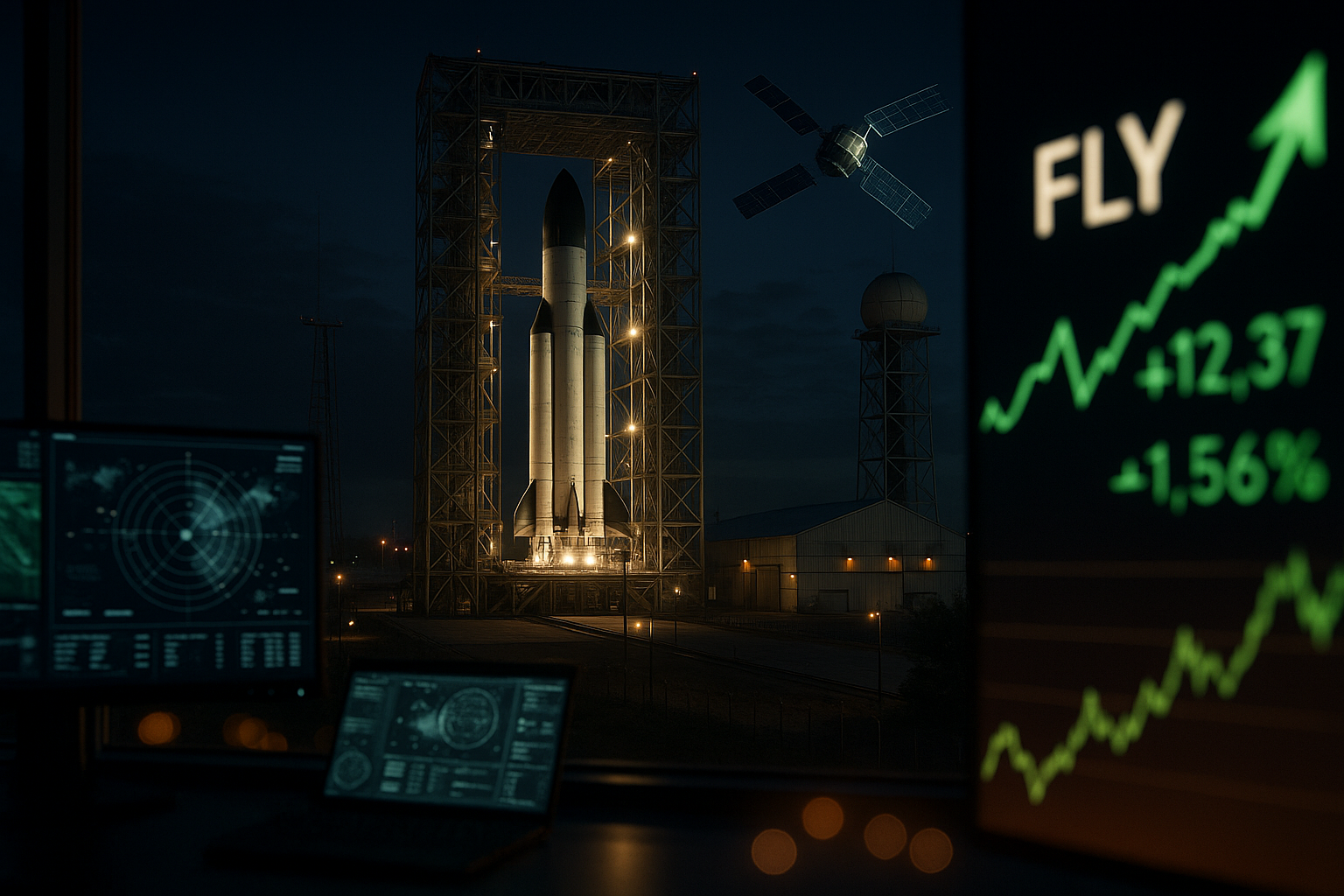

Market Reaction & Stock Impact

Shares of Firefly (ticker FLY) jumped in response. Reports indicate the stock rose by 8–9 % on the day of the announcement. The move is interpreted by many as the market rewarding strategic depth, investors seeing Firefly’s shift from pure-play launch hardware to defense-augmented capabilities.

Analysts have taken notice: Jefferies, for example, rates the transaction as strengthening Firefly’s trajectory beyond hardware alone. The stock’s prior volatility, exacerbated by a recent rocket test failure, makes consistency and execution critical for validating this new narrative.

Strategic Rationale & Operational Synergies

Blending Launch, Space & Defense

Firefly’s core business has centered on small- to medium-lift launch vehicles, lunar landers (like its Blue Ghost craft), and in-space services. SciTec brings critical defense capabilities, missile warning, tracking, intelligence surveillance, data analytics, that complement Firefly’s hardware.

This vertically integrated model enables Firefly to propose end-to-end solutions: delivering payloads, managing onboard systems, processing data in orbit or on ground, and offering defense-grade control and analytics.

Growth Levers & Competitive Edge

- Defense contracts & margins: SciTec already holds lucrative contracts (e.g. with the U.S. Space Force). Firefly can more credibly compete for national security payloads and command systems.

- Differentiation from pure launch peers: While many space firms compete on cost per kg, Firefly now competes on systems integration, tying defense, software, and satellite services.

- Equity alignment: By funding a portion of the deal with equity, Firefly’s long-term success is tightly tied to performance, setting incentives for SciTec’s integration to add real value.

Risks & Execution Challenges

Integration Complexity & Cultural Fit

Merging a software-driven defense firm with a hardware-led launch business is nontrivial. Different engineering cycles, security protocols, compliance regimes, and corporate cultures must align. Any misstep could dilute strategic value.

Capital Strain & Dilution

The equity portion of $555 million introduces dilution risk for existing shareholders. Moreover, Firefly may need to manage its balance sheet carefully to fund synergies while maintaining launch operations, R&D, and capital commitments.

Technical & Operational Setbacks

Firefly has recently faced testing failures. In September, a first-stage booster underwent a testing mishap that raised concerns over reliability. Execution misfires could undermine confidence in the combined company’s credibility.

How Investors Might Position

- Core equity play in FLY

Investors bullish on defense and space integration may see Firefly as a rare cross-domain play, but upside depends heavily on execution. - Pair trades & hedges

Consider hedging exposure given the technical risks and dilution potential. Pairing FLY with more stable defense equities may mitigate downside. - Watch contract announcements

Key inflection points will be new contracts or announcements that substantiate the deal’s strategic vision, especially defense wins. - Monitor integration updates

Operational milestones (software migration, system integration, joint offerings) will be critical in validating the thesis.

In summary, the Firefly SciTec acquisition is a bold move for the company: scaling from pure launch into defense and data-driven software systems. The FLY stock reaction is positive, but the path ahead demands rigorous execution, disciplined capital management, and synergy realisation. If Firefly can stitch together launch, space, and defense under one canopy, it may redefine expectations for integrated aerospace firms.

Other News

The Role of Intelligent Forex Trading Systems in Optimizing Algorithmic Trading Performance

By Tredu.com · 5/20/2026

How Machine Learning Forex Trading Bot Enhances Predictive Accuracy in Forex Markets

By Tredu.com · 5/20/2026

FinancialMarkets.media granted the Official Google Partner certification

By Tredu.com · 5/20/2026